When evaluating the program, it’s important to separate what’s fraudulent from what’s just bad policy.

There's a lot of confusion about what's happening in Washington. Here's what I think it means for the SBA.

This year, we are going to invest in employee-training programs. It’s an important initiative, but tracking its results, and its ROI, would be difficult.

But the problems they see are not always caused by the SBA.

One of my clients has a tough decision to make: Is he willing to use his home as collateral?

But we did learn some important things, and I’m optimistic that 2025 will be better.

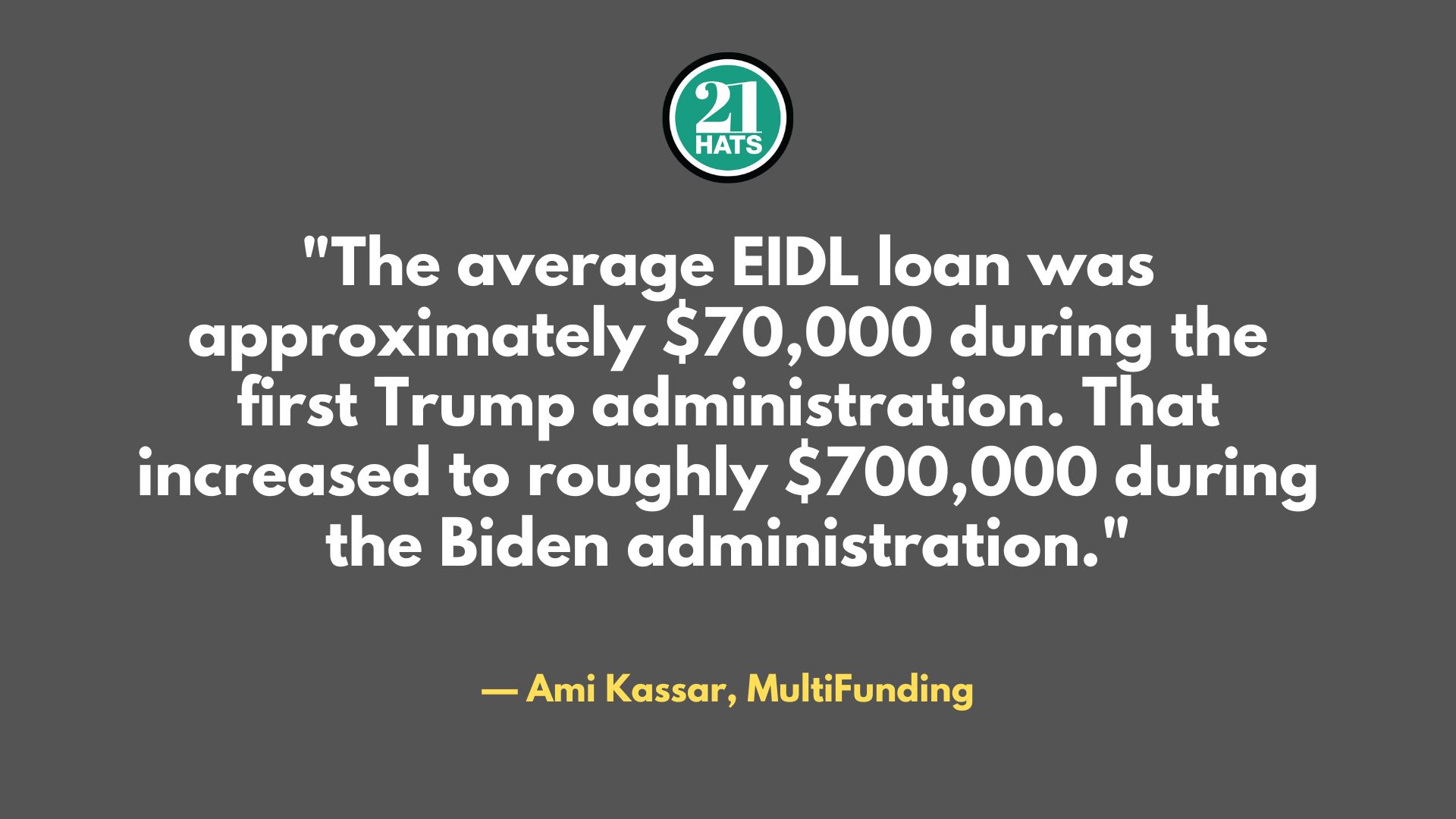

Defaults on Covid-era lending have left a cloud hanging over the agency. Can it learn from its mistakes without forfeiting its mission?

I was surprised to learn how many business owners leave money on the table when dealing with their bank.

The top 100 SBA lenders are far from interchangeable. They come in many different shapes, sizes, and competencies. And they also come and go.

We will have peer-group conversations on the issues you want to discuss. We will tour local businesses. We will eat good food. We will build relationships. And we’ll leave inspired.